Navigating Financial Transitions: A Comprehensive Guide on Converting a Joint Bank Account into a Single Account

Introduction:

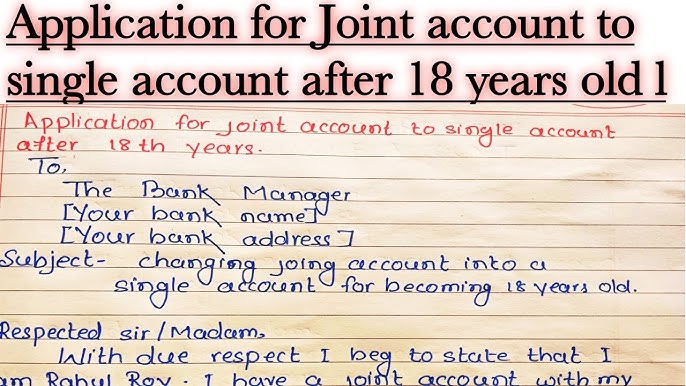

Life is dynamic, and financial circumstances often evolve. One such change may involve transitioning from a joint bank account to a single account. Whether due to changes in relationships, financial independence, or a need for personal financial management, this comprehensive guide will walk you through the steps and considerations involved in converting a joint bank account into a single account. From understanding the implications to navigating the administrative processes, we aim to provide you with a roadmap for this financial transition.

Section 1: Assessing the Need for Change

1.1 Communication and Agreement:

- Open and honest communication is essential when considering this change.

- Ensure that both account holders are on the same page and agree on the reasons for converting the joint account into a single account.

1.2 Relationship Changes:

- Evaluate changes in relationships, such as divorce, separation, or changes in financial responsibilities.

- Consider the impact of these changes on joint financial management and whether a single account is more suitable.

Section 2: Understanding the Implications

2.1 Legal and Financial Implications:

- Research the legal and financial implications of converting a joint account into a single account.

- Be aware of any contractual obligations or potential fees associated with account changes.

2.2 Asset Division:

- In the case of relationship changes, understand the implications of asset division and how it may affect joint accounts.

- Seek legal advice if necessary to ensure a fair and legal separation of financial assets.

Section 3: Notifying the Bank

3.1 Contacting the Bank:

- Initiate the process by contacting your bank. Most banks offer various channels, including in-person visits, phone calls, or online platforms.

3.2 Account Holder Consent:

- Confirm whether the consent of both account holders is required to convert the joint account into a single account.

- Be prepared to provide identification and relevant documentation.

3.3 Bank Policies and Procedures:

- Familiarize yourself with the bank’s policies and procedures regarding account changes.

- Inquire about any forms or documentation required for this process.

Section 4: Closing the Joint Account

4.1 Settling Outstanding Transactions:

- Ensure that all outstanding transactions, including checks and direct debits, are settled before closing the joint account.

- Update recurring payments with the new account details if necessary.

4.2 Transferring Funds:

- Decide on the equitable division of funds in the joint account.

- Transfer the agreed-upon portion to the new single account.

4.3 Closing the Account:

- Follow the bank’s procedures for closing the joint account.

- Obtain confirmation in writing or digitally that the joint account has been closed.

Section 5: Opening a Single Account

5.1 Choosing a Bank:

- Evaluate different banks and their offerings to find a suitable institution for your new single account.

- Consider factors such as fees, services, and convenience.

5.2 Single Account Options:

- Select the type of single account that aligns with your financial needs, whether it be a savings account, checking account, or a combination of both.

5.3 Updating Personal Information:

- Provide the necessary identification and documentation to open the new single account.

- Update any personal information, such as address or contact details, during the account setup process.

Section 6: Updating Financial Accounts and Services

6.1 Direct Deposits and Withdrawals:

- Notify employers, pension providers, or any other entities of your new account details for direct deposits.

- Update billing information for automatic withdrawals.

6.2 Creditors and Loan Providers:

- Inform creditors and loan providers of your account change to avoid any disruptions in payments.

- Update account details for loans, mortgages, or credit cards.

6.3 Government Agencies:

- If applicable, notify government agencies of your account change, especially if you receive benefits or tax refunds directly into your account.

Section 7: Monitoring and Managing the Single Account

7.1 Budgeting and Financial Planning:

- Develop or revise your budget and financial plan based on the changes in your financial structure.

- Utilize personal finance tools or apps to track your spending and savings goals.

7.2 Emergency Fund and Contingencies:

- Ensure that your single account includes an emergency fund to cover unexpected expenses.

- Review and adjust your financial safety nets as needed.

Section 8: Seeking Professional Advice

8.1 Financial Advisors:

- Consider seeking advice from a financial advisor, especially if the transition involves complex financial scenarios or legal implications.

- An advisor can provide guidance on asset management, tax implications, and long-term financial planning.

8.2 Legal Counsel:

- In cases of relationship changes, consult with legal professionals to understand the legal implications of converting joint accounts into single accounts.

- Ensure that any legal documents, such as wills or powers of attorney, are updated accordingly.

Conclusion:

Converting a joint bank account into a single account is a significant financial transition that requires careful consideration and planning. By assessing the need for change, understanding the implications, and navigating the administrative processes, you can streamline the transition and ensure a smooth financial journey. Open communication, adherence to legal requirements, and a proactive approach to managing accounts will empower you to navigate this change successfully. Remember to seek professional advice when needed and, most importantly, prioritize financial well-being and stability.